Introduction: The recent upstream pure benzene market continues to rise, and the cost side forms strong support for the caprolactam market, and the caprolactam market follows the upward trend. The main supporting power of the late market is still from the cost side, it is expected that the caprolactam market will run strongly in the near future, and the continuing power of rising costs and the downstream transmission process will be concerned in the later stage.

Since July, the pure benzene market has been boosted by multiple factors such as the rise in crude oil, the improvement of its own supply and demand pattern and the impact of consumption tax related news on ethylbenzene demand, and the pure benzene market has continued to rise. Sinopec pure benzene listed price since the beginning of the month 6200 yuan/ton rose to the current 6950 yuan/ton.

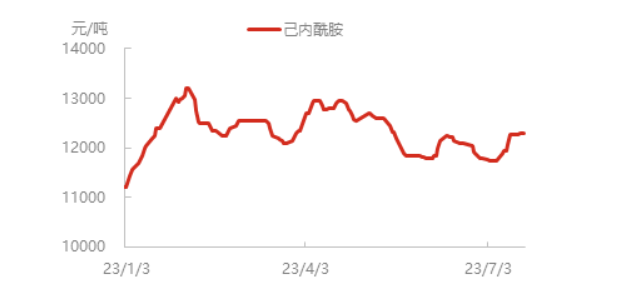

The price of pure benzene continues to rise, the cost of caprolactam enterprises has increased, and the price of products has risen. At present, the spot price of caprolactam in East China has risen to near 12300 yuan/ton, and some caprolactam shipments in the north are slightly tight, and the downstream procurement enthusiasm is OK in the upward process, and the polymerization factory basically follows up as needed.

With the restart of Luxi Chemical Industry, Cangzhou Xuyang Phase I and other devices, caprolactam capacity utilization rate increased to 81.35%, except for some long-term parking devices are still in the parking state, other devices are basically running normally. However, due to the low inventory of caprolactam in the early stage, coupled with the current market is in an upward trend, and the downstream procurement enthusiasm preference, the northern part of the supply is still slightly tight.

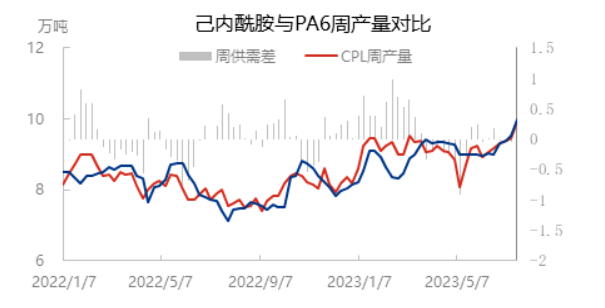

PA6 polymerization capacity utilization rate has recently risen synchronously, on the one hand, the demand preference of high-speed spinning downstream continues to support the start of polymerization, on the other hand, the early parking device of Luxi Chemical has gradually restarted, and the PA6 capacity utilization rate has increased to near 76%, and the weekly slicing output and caprolactam weekly output have increased synchronously to close to 100,000 tons.

The downstream nylon filament load remains stable, and the current domestic average nylon filament load is about 79.5%. The comprehensive operating rate of chemical fiber weaving in Jiangsu and Zhejiang regions was 63.47%, down 0.40% from last week. Weaving started a small decline, but the overall change is little, the current terminal weaving is not affected by power rationing, downstream users are mostly in the waiting and wait-and-see stage, waiting for domestic and foreign trade new single centralized release.

In summary, the current caprolactam market support power comes from the cost side, caprolactam and PA6 polymerization capacity utilization rate increased synchronously, caprolactam supply and demand are basically balanced, it is expected that the caprolactam market is strong in the near future. The downstream spinning field is relatively stable, and there is no significant change in the raw material demand expectation, and the high-speed spinning field is still able to follow up. The conventional textile field is still slow to follow up, and with the increase of supply and competitive pressure, there is still resistance to the downward transmission of high prices. In the later stage, it is still necessary to pay attention to the continuous power of cost increase and the transmission process to the downstream.

Post time: Jul-27-2023